ch1.fundamentals_of_trading_system

Differences Between High-Frequency Trading (HFT) and Regular Trading

-

Speed and Automation:

- HFT:

- Shortest feasible data latency.

- Highest level of automation.

- Relies on algorithmic and automated trading.

- Uses precise algorithms to find trading opportunities and execute orders.

- Employs fast connections for rapid transactions, cancellations, and modifications.

- Regular Trading:

- Slower execution speeds.

- Less reliance on automation.

- More human intervention in trading decisions.

- HFT:

-

Market Preferences:

- HFT:

- Operates in highly automated and integrated trading platforms.

- Prefers exchanges with advanced technologies.

- Regular Trading:

- Operates across various platforms, not necessarily requiring high levels of automation.

- HFT:

Exchanges Investing in HFT Technologies

- NASDAQ (New York City):

- First electronic stock exchange.

- Equities traded over a computerized network.

- High market capitalization with a focus on technology firms.

- New York Stock Exchange (NYSE) (New York City):

- Largest equity market exchange.

- Owned by Intercontinental Exchange, Inc. (ICE) since 2013.

- London Stock Exchange (LSE) (London, UK):

- Largest stock exchange in Europe.

- Principal exchange for company stocks and bonds in the UK.

- Tokyo Stock Exchange (TSE) (Tokyo):

- Largest stock exchange in Japan.

- Operated by Japan Exchange Group.

- Home to major Japanese corporations like Toyota and Honda.

- Chicago Mercantile Exchange (CME) (Chicago):

- Futures and options exchange.

- Trades in sectors like agriculture, energy, stock indices, and foreign exchange.

- Direct Edge (Jersey City):

- Significant market share in the US stock market.

- Merged with BATS Global Markets, which was later acquired by CBOE Holdings.

- CBOE Options Exchange:

- Largest options exchange.

- Contracts based on individual stocks, indexes, and interest rates.

Regulatory Controls

- Exchanges Control Measures:

- Trading limitations.

- Transparency of trading systems.

- Types of accepted financial instruments.

- Constraints imposed by security issuers.

- Order Size Issues:

- Large trades can impact the market significantly.

- Use of Alternative Trading Systems (ATS) like dark pools to minimize impact.

Dark Pools and HFT

- Dark Pools:

- Less regulated compared to traditional exchanges.

- Not required to be transparent.

- Around 30 dark pools in the USA, representing a quarter of US consolidated trading volume.

- Beneficial for HFT due to speed, automation capability, and reduced fees.

- Less common in regular trading due to different requirements and regulations.

Effect of Dark Pools

- Characteristics:

- Opaque and anonymous: buy and sell orders are not displayed.

- No visibility on order size: reduces market impact for large orders.

- Executes large orders at a fixed price, minimizing negative slippage.

- Obligated to notify deals post-trade, lacking pre-trade transparency.

Interaction Between HFT and Dark Pools

-

Investor Protection:

- Investors use dark pools to avoid HFTs' manipulative activities.

- HFTs find it challenging to identify large orders in dark pools through pinging.

- Lack of transparency allows traditional business practices to continue.

-

HFT Impact:

- Some dark pools encourage HFTs to increase liquidity and order fulfillment chances.

- HFTs benefit from speed, automation, and reduced costs.

- Responsible for decreased order sizes in dark pools due to pinging strategies.

Challenges and Regulations

-

Negative Impact of HFT Tactics:

- HFT strategies like pinging can locate hidden large orders, undermining dark pool benefits.

- Example: 2014 lawsuit against Barclays for misrepresenting dark pool activity, resulting in significant fines.

-

Preventive Measures:

- Dark pools can impose constraints to reduce predatory HFT behavior.

- Example: 2017 Petrescu and Wedow imposed minimum order size to minimize pinging.

Pros and Cons

-

Advantages of HFT in Dark Pools:

- Increased liquidity and faster execution.

- Beneficial for some dark pools despite the potential for predatory behavior.

-

Considerations for Investors:

- Understanding trading venues is crucial for making informed decisions.

- Balancing the benefits of HFT liquidity with the need for transparency and fair practices.

Who Trades HFT?

-

Participants:

- Proprietary Trading Firms:

- Dominated by businesses focusing solely on trading for profit.

- Major players include KCG Holdings (merger of Getco and Knight Capital) and trading desks of major banks.

- Multi-Service Broker-Dealer Proprietary Trading Desks:

- Engage in HFT but constitute less than half of the HFT participants.

- Hedge Funds:

- Account for the remaining portion of HFT players.

- Electronic Communication Networks (ECNs):

- Facilitate HFT by providing platforms for trading.

- Inter-Dealer and Inter-Broker-Dealer Markets:

- Utilize HFT for executing trades among themselves.

- Proprietary Trading Firms:

-

Scope of HFT:

- Covers a wide range of financial products:

- Stocks

- Derivatives

- Index funds

- Exchange-Traded Funds (ETFs)

- Currencies

- Fixed-income instruments

- Covers a wide range of financial products:

-

New Trading Venues:

- Venues like Dealerweb's OTR Exchange and IEX provide safe environments for dealers to execute trades.

- HFT firms provide liquidity in these venues.

-

Market Influence:

- HFT firms are major players in the financial markets.

- Capture significant retail flow, with firms like Citadel controlling a large portion.

Requirements to Start High-Frequency Trading (HFT)

-

Fast Computers:

- Focus on single-core throughput.

- Strategies may not rely heavily on parallelism.

-

Exchange Proximity (Co-Location):

- Co-locate production servers with exchange servers in the same data centers to reduce latency.

- Ensures equal cable lengths between trading systems and servers to maintain fairness.

- Co-location fees are regulated to ensure reasonable pricing and fairness among participants.

-

Low Latency:

- Latency: Time for data to reach the trader's computer, for the order to be placed, and accepted by the exchange.

- Importance of low-latency or ultra-low-latency technology to execute orders quickly.

- Use of specialized hardware to minimize data transfer latency.

-

Computer Algorithms:

- Core of algorithmic trading (AT) and HFT.

- Designed to process real-time data feeds and execute trades based on predefined strategies.

-

Real-Time Data Feeds:

- Essential for making timely trading decisions.

- Direct impact on earnings and trading effectiveness.

Domain of Applications and Vocabulary for HFT Strategies

-

Asset Classes:

- HFT strategies apply to various asset classes, including:

- Stocks

- Futures

- Bonds

- Options

- Foreign Exchange (FX)

- Cryptocurrencies (different speed considerations due to settlement time)

- HFT strategies apply to various asset classes, including:

-

Liquidity:

- Definition:

- The willingness of market participants to trade a specific asset.

- Depth:

- Number of price levels for an asset.

- A "deep" book has many levels.

- Volume per Layer:

- Amount of assets available at each price level.

- A "broad" book has high volume per layer.

- Liquid Market:

- Characterized by a deep and broad book, making it easier to buy or sell assets.

- Current Issues:

- Cryptocurrency exchanges often struggle with liquidity.

- Definition:

-

Tick-by-Tick Data and Data Distribution:

- Data Generation:

- Orders generated every microsecond, resulting in massive data volumes.

- Storage:

- Key for analyzing and creating models for trading strategies.

- High-Frequency Data:

- Comprises thousands of ticks (price changes) per trading day in liquid markets.

- Fat Tail Distributions:

- Indicates potential for large losses, requiring strategies to account for these risks.

- Market Data Categories:

- Volatility Clustering:

- Large changes follow large changes, and small changes follow small changes.

- Long-Range Dependency (Long Memory):

- Statistical dependence between two points decays slowly over time or distance.

- Volatility Clustering:

- Data Generation:

-

Liquidity Rebates:

- Maker-Taker Model:

- Makers:

- Provide liquidity by placing limit orders, earning rebates from exchanges.

- Takers:

- Take liquidity by placing market orders, paying fees to exchanges.

- Makers:

- Rebate Significance:

- Small per-share rebates can add up to significant amounts over millions of trades.

- Many HFT strategies aim to maximize liquidity rebates.

- Maker-Taker Model:

-

Matching Engine:

- Definition:

- Software that matches buy and sell orders on an exchange.

- Ensures efficient operation of the exchange by continuously matching buyers and sellers.

- Location:

- Housed on the exchange's computers.

- HFT Importance:

- Proximity to the matching engine is critical for reducing latency.

- Definition:

-

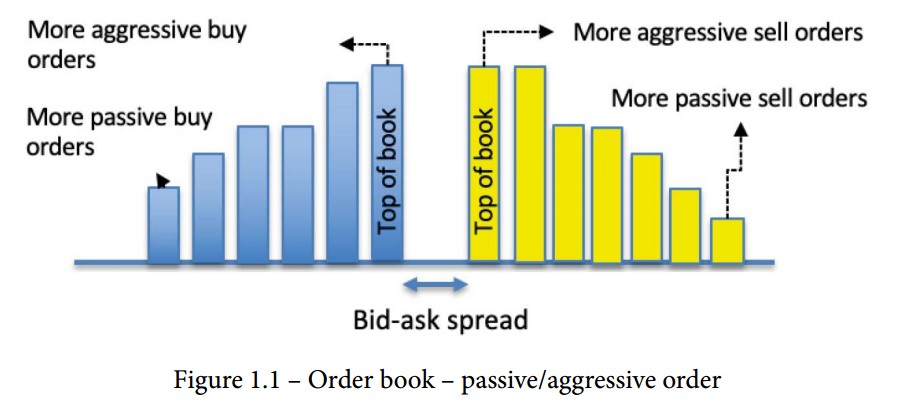

Market Making:

- Definition:

- Placing limit orders to provide liquidity and capture the bid-ask spread.

- Market Taker/Maker:

- Market Taker:

- Places aggressive orders likely to be matched.

- Removes liquidity from the market.

- Crosses the spread by placing buy orders at the ask price.

- Market Maker:

- Places passive orders not immediately matched.

- Provides liquidity to the market.

- Market Taker:

- Definition:

High-Frequency Trading (HFT) Strategies

HFT strategies are a subset of algorithmic trading strategies designed to execute orders within microseconds or nanoseconds. These strategies rely on cutting-edge technology to obtain and respond to market data faster than competitors. The key focus of HFT strategies is the "tick-to-trade" time, which is the response time to send an order after receiving market data. To achieve this, HFT strategies must run on high-performance machines and be co-located with exchange servers to minimize latency.

Market-Making Strategies

-

Market Making as a Service:

- Trading corporations provide market-making services on exchanges.

- Market makers facilitate the matching of buyers and sellers.

- Profit is generated from the spread (difference between buy and sell offers).

-

Operational Mechanics:

- Continuous offers to buy and sell securities are maintained.

- Aim to match every purchase with a sale and every sale with a purchase to reduce the risk of holding stocks.

- Example: If a stock trades at $100, a market maker might set buy offers at $99.50 and sell offers at $100.50.

- If they are successful in finding both a buyer and a seller, it allows those who want to sell right now to do so even if no one else wants to purchase, and vice versa.

- Market makers, in other words, supply liquidity—they make trading simpler.

-

High-Frequency Trading (HFT):

- Many HFT firms use market-making strategies.

- They quickly adjust quotations and reduce spreads to out-compete others.

- Scale operations to massive quantities despite lower per-trade profits.

- HFT technology can also be used for:

- Arbitrage: Profiting from minor discrepancies between linked securities.

- Execution: Breaking up large trades to minimize market impact.

- Speed is the key element in HFT.

-

Order Flow Analysis in Market Making:

- Momentum: Large volumes of buy and sell orders can drive market prices.

- Order Size: Analyzing the size of orders (small, medium, or large).

- Exhaustion of Momentum: A decrease in order flow may indicate a price reversal.

Scalping

-

Definition:

- Scalping is a trading method that capitalizes on small price movements.

- Involves quick reselling for fast profits.

- Generates large volumes from tiny profits.

-

Key Characteristics:

- Requires a tight exit strategy to prevent a single major loss from erasing all small gains.

- Essential tools: live feed, direct-access broker, and the endurance to perform many trades.

-

Concept:

- Most stocks complete the first stage of a trend, but future movements are uncertain.

- Scalping aims to profit from numerous minor transactions.

- Contrasts with the "let your gains run" approach, which maximizes trade size rather than quantity.

-

Execution:

- Focuses on increasing the number of winning trades while compromising on the size of gains.

- Long-term traders may achieve significant profits with a win rate of 50% or less, as their wins outweigh losses in size.

Statistical Arbitrage

-

Definition:

- Profits from price discrepancies based on anticipated values given by statistical models.

- Known as "stat arb," it focuses on short-term price differences in the same security across different venues or related securities.

-

Relation to Efficient Market Hypothesis (EMH):

- EMH states financial markets are informationally efficient, meaning prices reflect all known information.

- Market fluctuations occur due to liquidity needs, not just fundamental news.

- Large institutional trades affect prices due to liquidity, not information.

-

Liquidity Impact:

- Investors hedge or sell aggressively when overexposed, impacting prices.

- Liquidity seekers often pay a premium to exit positions, benefiting liquidity providers.

- Profiting from this violates efficient market theory but is the basis of statistical arbitrage.

-

Mechanics:

-

Algorithmic Trading: Well-suited for stat arb due to the need for rapid execution.

- Tracks all trading venues for a security.

- Buys in lower-priced markets and sells in higher-priced ones to profit from discrepancies.

- Operates within milliseconds.

-

Linked Securities:

- Examples: An index and a stock within it, or stocks within the same sector.

- Requires extensive historical data to estimate usual connections.

- Buys or sells when there's a deviation from the norm.

-

Latency Arbitrage

-

Definition:

- Latency arbitrage exploits the speed differences in data processing among market players.

-

Mechanics:

- Utilizes high-speed technologies:

- High-speed fiber optics.

- Superior bandwidth.

- Co-located servers.

- Direct-price feeds from exchanges.

- High-frequency traders (HFT) use these technologies to place trades faster than others.

- Utilizes high-speed technologies:

-

Hypothesis:

- The National Best Bid and Offer (NBBO) feed, which aggregates data from all US stock exchanges, is slower than the direct data feeds available to HFT traders.

- HFT algorithms read transaction data faster than the Securities Information Processor (SIP) feed (the consolidated US stock exchange price feed).

-

Advantages:

- HFT programs can see prices slightly ahead of the SIP feed.

- This advance information allows HFT traders to predict price movements before other market participants.

-

Tools and Technologies:

- High-speed fiber optics.

- Superior bandwidth.

- Co-located servers (servers located close to exchange servers).

- Direct data feeds from stock exchanges.

Impact of News

-

Role of Information:

- Central to financial decision-making.

- Used by algorithmic trading systems for generating trading decisions.

-

Information-Driven Strategies:

- Algorithms analyze news reports from major organizations and social media.

- Algorithms buy or sell based on news impacting market prices.

-

Technological Integration:

- News agencies package press releases with predefined keywords for easy computer analysis.

- Algorithms act on keywords indicating positive or negative events.

- News providers place reports on servers in major financial centers to reduce data transfer time.

- Additional fees are charged for these expedited news services.

-

Examples and Implications:

- Social media’s growing role in information-driven trading.

- 2013: Hacking of the Associated Press Twitter feed led to a false tweet about a bomb in the White House, causing a rapid global market plunge as algorithms sold off in response to the news.

Momentum Ignition

Momentum ignition is a trading tactic where traders aim to start a price movement by creating a false impression of market momentum. The strategy involves using a series of actions to trigger other traders or algorithms to react and trade, which in turn drives the price in the desired direction.

Key Concepts

-

Deceptive Order Placement:

- Initial Order: The trader places a significant number of orders into the market. These orders are designed to create the appearance of increased trading volume.

- Order Cancellation: After the initial orders are placed, they are quickly canceled. This action creates a false sense of high trading activity or volatility.

-

Price Movement Induction:

- The large volume of orders and their subsequent cancellation can lead other market participants to believe that a significant price movement is imminent.

- This perception can prompt other traders to place their own trades, believing they need to act quickly to benefit from the anticipated price change.

-

Execution of Targeted Position:

- Before the momentum ignition starts, the trader takes an initial position in the stock that does not significantly affect the market.

- The real trading position is typically set up quietly to avoid drawing attention.

-

Ignition Phase:

- Once the initial position is established, the trader begins the momentum ignition phase by sending and canceling a large volume of orders.

- The goal is to simulate a sudden surge in trading activity, which can trigger other traders to follow suit.

-

Profit Realization:

- As the momentum ignition causes the price to move, the trader can exit their initial position at a profit.

- The price movement becomes a self-fulfilling prophecy: the perception of movement encourages further trading, which drives the price as anticipated.

Techniques and Tools

- Order Types: Momentum ignition strategies often rely on specific order types that can be quickly executed and canceled.

- Algorithmic Trading: Successful execution of momentum ignition requires sophisticated algorithms capable of placing and canceling large numbers of orders rapidly.

- Market Impact: The strategy exploits the market’s response to perceived activity rather than actual changes in fundamental value.

Risks and Considerations

- Regulatory Risks: Momentum ignition can be viewed as manipulative and may be subject to regulatory scrutiny or legal action.

- Market Impact: While the strategy aims to create a price movement, it can also lead to unexpected consequences or market reactions.

- Ethical Concerns: The use of such strategies raises ethical questions about market fairness and transparency.

Rebate Strategies

Rebate strategies involve leveraging the fee structures provided by exchanges to optimize trading costs and potentially gain financial advantages.

-

Market Order vs. Limit Order Fees:

- Market Orders: Traders who execute market orders pay a fee to the exchange for taking liquidity from the market. Market orders are typically filled immediately but come at a cost.

- Limit Orders: Traders who place limit orders are adding liquidity to the market. Exchanges often offer rebates to these traders as an incentive to provide liquidity. This is because limit orders contribute to the market depth and help in price discovery.

-

Rebate-Based Trading:

- Traders who engage in high-frequency trading (HFT) often utilize rebate strategies to reduce their trading costs. By placing and maintaining limit orders, they receive rebates from the exchange, which can offset the costs of trading.

- This type of trading is appealing because it allows traders to build liquidity in the market while potentially earning rebates.

-

Maker-Taker Pricing Model:

- Maker Pricing: Traders who provide liquidity (e.g., by placing limit orders) are often referred to as “makers” and may receive rebates.

- Taker Pricing: Traders who remove liquidity (e.g., by placing market orders) are known as “takers” and usually pay fees.

-

Trader-Maker Pricing:

- In contrast to the standard model, some exchanges may offer a reversed pricing structure where market order traders (takers) receive rebates, and limit order traders (makers) pay fees. This can incentivize traders to place market orders, which can impact the market dynamics.

Ping Trading

Ping trading is a strategy used to detect large orders and is often associated with high-frequency trading.

-

Objective:

- Detect Large Orders: Ping trading involves placing small orders, usually for a minimal quantity (e.g., 100 shares), to gather information about the presence of large orders in the market.

- Market Impact Reduction: By breaking down large orders into smaller parts, traders aim to reduce the impact of their trades on the market.

-

Strategy:

- Small Marketable Orders: Traders place these small orders to test the market and see how large orders are distributed.

- Monitoring Responses: The responses to these small orders can provide insights into the presence of large orders in the market or dark pools.

- HFT Reaction: High-frequency trading firms may use these pings to identify and exploit large orders placed by other traders.

-

Implications:

- Market Awareness: Ping trading can help traders gain insights into large orders and adjust their strategies accordingly.

- Market Impact: The strategy may be used to mitigate the impact of large trades, but it can also alert other market participants to the presence of large orders, potentially leading to adverse market reactions.

- Ethical and Regulatory Concerns: Ping trading can be seen as a form of market manipulation or baiting, and its use may be subject to regulatory scrutiny.

Illegal Activities

Front-Running

-

Definition:

- Front-running involves placing an order based on non-public information about upcoming orders. This typically means executing a trade before a large order is publicly known, with the intent of profiting from the anticipated price movement caused by the large order.

-

Legal Status:

- Front-running is considered illegal under regulations enforced by the SEC and FINRA. It is viewed as unethical because it exploits confidential information for personal gain.

-

High-Frequency Trading Context:

- In the context of high-frequency trading (HFT), front-running can occur when HFT firms use sophisticated algorithms to detect large incoming orders and place their trades ahead of these orders to profit from the anticipated price changes. This practice, even if not explicitly illegal, is under scrutiny by regulators who are concerned about its potential impact on market fairness.

Spoofing

-

Definition:

- Spoofing involves placing orders with no intention of executing them, with the goal of misleading other market participants. The purpose is to create a false impression of supply or demand to influence market prices.

-

Legal Status:

- Spoofing is illegal and has been specifically targeted by regulations such as the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. The practice violates regulations that prohibit orders intended to mislead the market.

-

Mechanism:

- A trader may place large orders to create a false sense of demand or supply, only to cancel these orders before they are executed. This can prompt other traders to act on the misleading information, resulting in market manipulation.

Layering

-

Definition:

- Layering is a variation of spoofing where orders are placed at multiple price levels to create an illusion of high interest in a particular security. The aim is to mislead other market participants about the true level of supply or demand.

-

Legal Status:

- Like spoofing, layering is illegal and is prohibited under FINRA rules. It is considered a form of market manipulation because it creates a deceptive appearance of market depth.

-

Technology and Speed:

- The rapid advancement in trading technology means that layering can occur in fractions of a second, making it difficult to detect and prevent. Despite being outlawed, some less-regulated exchanges or markets may still see the use of these strategies.

Regulatory and Ethical Considerations

-

Regulatory Actions: Regulatory bodies are increasingly focusing on these illegal practices to ensure market integrity and fairness. Violations can lead to severe penalties, including fines and criminal charges.

-

Less Regulated Markets: While these practices are banned in regulated markets, they may still occur in less regulated or emerging markets, such as certain cryptocurrency exchanges.

-

Impact on Market Integrity: These strategies undermine market integrity and can harm individual investors and the overall financial system. Continued vigilance and enforcement are essential to maintaining fair and transparent markets.